Turning 65 is a huge milestone for most people.

It’s definitely a reason to celebrate but it’s also a time to transition to a new chapter in your life. You’re thinking about retirement in beautiful Tucson, preserving and protecting your finances, making sure your children are off to a good start in their lives, and many other important life issues.

In addition to all of these changes, one of the most important things that happens when you turn 65 is that you’re now eligible for Medicare. Some people are eligible at an earlier age if they have a qualifying condition, but for the vast majority of Americans, 65 is the age when Medicare kicks in.

Medicare offers you a lot of benefits, however, it can also result in a lot of uncertainty and questions about coverage, costs, plan choices, and more. Tucson continues to grow and doctor and hospital networks continue to change, so it’s important to work with someone local who deeply understands the Tucson Medicare market.

Our team at Medicare Health Benefits have been helping seniors turning 65 in Tucson since 1996, we have helped thousands understand what to do with Medicare when they turned 65 and became eligible. Are you Native American? If so, we have an in house specialist that currently supports 23 tribes across Arizona and New Mexico. Learn more about health insurance plans for Native Americans.

We’ve put together this guide to answer a lot of the questions about what happens when you turn 65 and become eligible for Medicare coverage.

Medicare Plans by County in Arizona

Unless you choose a Medicare supplement, Medicare Advantage plans are county specific. Below is a summary of Medicare Advantage plans by county across the state of Arizona.

Turning 65: Medicare Basics

As you get older, there’s a good chance you’ve already started to learn about Medicare and how it can benefit you. You’ve probably gotten some things in the mail, chatted with friends at work before retirement, or done some online research to try and wrap your head around it.

If you’re not well versed in Medicare basics, you need to take a couple of minutes to get a good overview of the program and some of the key terminology that will impact you.

Here’s a good place to start:

What is Medicare?

Medicare is a federal health insurance program that helps people 65 and over, and those who are under 65 and meet certain qualifying conditions. You are eligible to enroll regardless of your current health status, income or medical history.

The Centers for Medicare and Medicaid Services (CMS) is the federal agency that administers Medicare. The program is funded in part by Social Security and Medicare taxes that you pay on your income throughout your working life (40 working quarters).

Some people also fund Medicare by paying premiums for services. The balance of Medicare is covered by the federal budget. Our team can help you understand how much it will cost you during your plan review.

Medicare is divided into four main parts which are A, B, C, and D.

Original Medicare

Medicare Part A and Medicare Part B are often referred to as Original Medicare. These two parts form the foundation of coverage for most people.

- Part A covers hospital-related services such as inpatient care, skilled nursing facility care, hospice, and home health care. This is what Tucson hospitals like Banner University, Carondelet Marana, St. Mary’s, Northwest and others are billing when you use their services.

- Part B covers medically necessary services and supplies that are needed to diagnose your illness or condition. That can include clinical research, mental health treatment, ambulance services, lab tests, and durable medical equipment (i.e., wheelchairs, walkers, canes, nebulizers, blood sugar monitors and test strips, CPAP devices, etc.)

For many people who enroll at 65, Part A is earned through working and there is no cost (but, it’s not free). You’ll need to pay a premium for Part B coverage more often than not.

In many cases, you’ll have deductibles, copays, and coinsurance for Original Medicare services and coverage.

Medicare Part C and Part D

While Original Medicare provides you with a solid foundation of coverage, it only covers 80%, and many people want to enjoy even lower costs through enhanced levels of coverage to reduce the 20% you’re responsible for.

After you enroll in Part A and Part B, you’re also eligible to choose to enroll in Medicare Part C and Part D which is your prescription drug plan.

Medicare Part C is commonly referred to as Medicare Advantage plans. CMS contracts with private health insurance providers to provide Medicare recipients with a higher level of coverage and services than in Original Medicare.

By law, Part C coverage must be equal to coverage in Part A and Part B, and many providers also include other benefits like vision, dental, hearing, fitness benefits, and more.

Not all Part C providers offer the same benefits, so you will need to do your homework or work with a local insurance agent to find the policy that best suits your needs, weighing added benefits vs. added premium costs. Medicare Health Benefits has been helping Tucson seniors make these choices since 1996, so we can certainly help you.

Part D is specifically related to coverage for prescription drug costs. Like Part C, Part D plans are also offered by private insurance companies.

You must already be enrolled in Original Medicare before you can enroll in a Part D plan. In many cases, Part C coverage will also include prescription drug coverage. It all depends on the plan. Again, this can get confusing which is why working with an agent is helpful.

Every Part D plan has a formulary. This is a published list of all the drugs covered under a particular policy.

Formularies will vary from each insurance company and this is something you need to consider when shopping for a Part D plan. And, these plans change every year, so between October 15th and December 7th every year is when you’ll have the opportunity to review the new plans available for the upcoming year.

Medicare Supplement Plans (Medigap)

Medicare supplement is your other choice.

Some people will opt to buy a Medicare Supplement insurance plan, also known as a Medigap plan for added coverage. These policies pay the gap between what Medicare covers and what your services will cost you.

Medigap policies are also sold by private health insurance providers. They are identified by a letter and labeled A, B, C, D, G, K, L, M, and N (plans E, F H, I, and J are no longer available).

For most states, coverage under a specific letter will be consistent because plans are regulated by the federal government.

For example, this means Plan N or Plan G coverage in Phoenix will be the same as Plan N coverage in Tucson, and so forth.

One thing to note is that Medicare Supplements do not have the network restrictions that Medicare Advantage plans have. For example, certain Medicare Advantage plans may only include one hospital system or another, but a Medicare Supplement would allow you to use any hospital in Tucson such as Banner, Northwest, Carondelet Marana, etc.

What is the Difference Between Medicare and Medicaid?

People often confuse Medicare and Medicaid with each other but they are completely different programs.

Here in Arizona, Medicaid is Arizona Health Care Cost Containment System (AHCCCS)

You are eligible for Medicare when you turn 65 and when you meet other qualifying criteria under 65, no matter what your income. AHCCCS Medicaid is need-based assistance for low-income adults and children in Arizona.

Medicare is a federal program but Medicaid is funded and administered by both the federal and state of Arizona. With Medicaid, all states must meet certain coverage criteria, but they also have the flexibility to add other benefits and set their own eligibility requirements.

In some cases, you can be eligible for both Medicare and Medicaid. This dual eligibility means both programs will work together to provide you with health coverage and lower costs. There are multiple options in Arizona for Medicare Advantage plans for people with Medicaid, and our team can help you navigate those choices.

How do I Enroll in Medicare when I turn 65?

When can I sign up for Medicare?

The best time to sign up for Medicare as you’re turning 65 is during your Initial Enrollment Period (IEP).

Your IEP begins three months before your 65th birthday, includes the month of your 65th birthday, and the three months afterward. If you don’t enroll during your IEP, your Medicare premium costs could be more later on. Some people don’t because they are still working, we can help you understand which path to take.

You have other opportunities to enroll or make changes as well.

If you want to make changes to your benefits after your IEP, you can do so during Medicare’s Annual Enrollment Period (AEP).

The annual enrollment period for Medicare (AEP) runs from October 15 through December 7 every year.

Some people can make changes during the Open Enrollment Period (OEP) which runs from January 1 through March 31 annually. It is for people who enrolled in a Medicare Advantage plan during the AEP and do not like their plan.

During the OEP, you can only change from one Medicare Advantage plan to another or drop your current Medicare Advantage plan.

The Special Enrollment Period (SEP) is for people who have special circumstances (such as a chronic illness or a major life change, like moving to a new state) and need to make a plan change. Your SEP can occur during any time of year.

How do I sign up for Medicare?

If you currently receive Social Security benefits, you will be automatically enrolled in Medicare Parts A and B the month you turn 65. You can decline Part B coverage if you don’t want to pay the added premium.

For Medicare Part C or Part D, or a Medicare Supplement plan, the best way to enroll is through an insurance agent.

You can also visit a Social Security office in person, or enroll by calling Social Security at 1-800-772-1213 (TTY 1-800-325-0778).

If you don’t qualify for automatic enrollment, you can sign up online at the Medicare website as long as you’re within three months of your 65th birthday. You have a 7-month window sandwiched around your 65th birthday known as your Initial Enrollment Period (IEP).

The Medicare enrollment application is fairly simple and generally takes less than 10 minutes to complete.

If you don’t enroll during your IEP, delaying your enrollment can result in a 10% Part B premium increase for every year you’re eligible but don’t enroll.

If you don’t select prescription drug coverage and later enroll, you may also face a Part D enrollment penalty as well.

Should I use an insurance agent?

As you have read, there is a lot to Medicare and only licensed insurance agents may legally discuss insurance benefits.

You’re sure to have questions and whatever coverage you decide to enroll in will not be any more expensive whether you speak to an agent or not. Federal law prohibits insurance agents from charging fees for processing Medicare plan enrollments.

You have nothing to lose and a lot to gain by speaking with an expert.

We have been serving the Tucson community since 1996 and Medicare is all we do. Our team would love to meet with you and help you understand Medicare.

Is it mandatory to sign up for Medicare at 65?

No. But it is the smart thing to do.

If you don’t sign up during your IEP, you could face premium penalty costs for the life of your coverage. You could also face delays in your coverage start date as well.

Always meet with an agent to help you determine the proper path that is best for you.

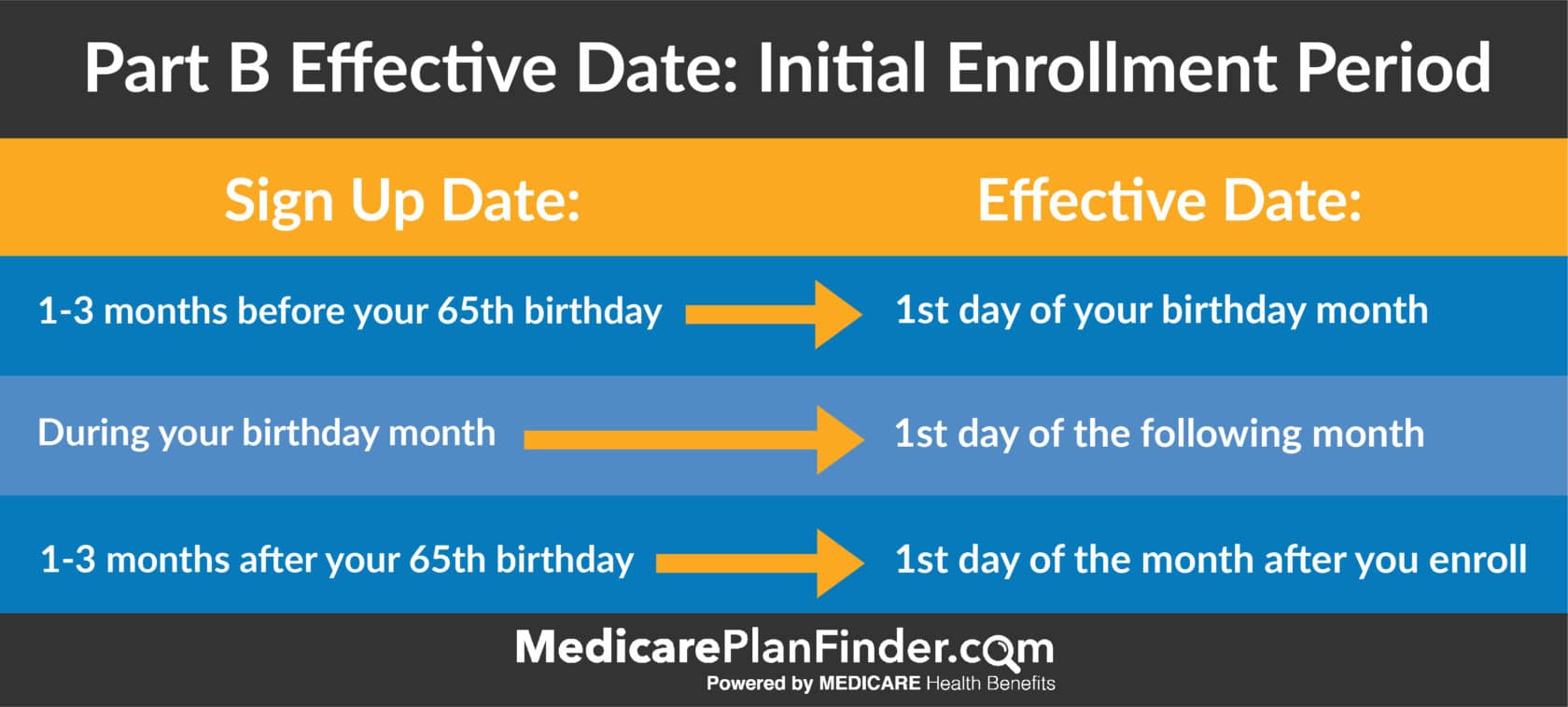

When will my Medicare coverage begin?

If you sign up during the three months before your 65th birthday, your Medicare coverage will begin on the first day of your birthday month.

However, if your birthday is on the first day of the month, your coverage will begin on the first day of the month before your birthday.

How much does Medicare cost?

If you have worked and paid Medicare taxes for at least 40 quarters (10 years), then you are entitled to free Part A coverage and your Part B premium is usually deducted from your social security check.

The standard Part B premium for 2025 is $185. You may pay a higher amount if your income is more than $87,000 a year, you could be charged up to $628.90 for your part b coverage. This is called IRMAA which is short for income related monthly adjustment amount. Your agent can work with you on determining how much your Part B premium will be.

You might also pay less due to the Social Security “hold harmless” provision that prevents premiums from exceeding Social Security benefits.

Part C and Part D premiums will vary based on the specific plans you choose and these change every year making annual reviews extremely important. You will want to work with a licensed agent to compare pricing and benefits.

What if I’m Still Working When I Turn 65?

If you’re still working when you turn 65, you may be able to delay your Medicare enrollment without facing a late enrollment penalty fee.

When you have coverage under a group plan through your employer with 20 or more employees, you don’t have to enroll in Medicare immediately.

Since most people who have worked through most of their lives will get premium-free Part A, there is usually no harm in enrolling regardless of your current employment status.

Also, if you’re still working at 65 and your employer has 20 employees, you can delay enrolling in Part B as a way to avoid paying the Part B premium.

In this case, if you leave your job or your employer stops offering coverage, you’ll have an eight-month special enrollment period to apply and won’t incur any premium surcharges for being late.

The special enrollment period also applies if you’re covered under your spouse’s employer-sponsored plan as well, as long as they have at least 20 employees.

Is Turning 65 the Only Time I Can Get Medicare?

You can get Medicare benefits if you’re under 65 in the following situations:

You have been receiving Social Security Disability Insurance (SSDI) checks for at least 24 months.

You have End-Stage Renal Disease (ESRD), and you are getting dialysis treatments or you have had a kidney transplant, and you’re eligible to receive SSDI, Railroad Retirement benefits or you or an immediate family member have paid Medicare taxes for a sufficient amount of time.

You receive SSDI benefits because you have Amyotrophic Lateral Sclerosis (ALS).

If you miss your IEP, you also have several possible enrollment periods to sign up at a later date.

Other Health Insurance Considerations

COBRA

When you leave your job, you’ll also have the option to keep your employer’s health plan through The Consolidated Omnibus Budget Reconciliation Act (COBRA).

This law gives workers and their families the right to continue with their employer’s health insurance for limited periods of time under circumstances such as voluntary or involuntary job loss, reduced working hours, a transition between jobs, death, divorce, and other life events.

The catch is that if you qualify, you could be required to pay the entire premium for coverage up to 102% of the cost to the plan.

Retiree Medical Coverage

Your employer may offer you retiree medical coverage after you leave your job. It is not the same as Medicare because it is coverage offered by your employer and not Medicare.

Not all employers offer retiree coverage. Since it isn’t required, your former employer can cancel or change your retiree plan at any time.

If you combine employer coverage with enrollment in Medicare, that provides you with the highest degree of safety.

Some retiree plans automatically stop when you turn 65 and become eligible for Medicare.

If your employer does not offer retiree coverage, retiring or losing your job gives you access to a Special Enrollment Period. This means you don’t have to wait for the Annual Enrollment Period to buy health coverage.

You will have 60 days from your last day of work to enroll in a Marketplace health plan. After those 60 days are over, you’ll have to wait until the AEP (October 15 – December 7) to buy a plan, and you will be charged a penalty fee for having a lapse in coverage.

FERS/CSRS Retirement

The CSRS, or Civil Service Retirement Act, became effective on August 1, 1920. It was replaced by the Federal Employees Retirement System (FERS) on January 1, 1987. Some people may still belong to CSRS. Both programs are for government employees only.

Both FERS and CSRS allow you to retire at age 62 if you have five or more years of service, or at age 60 if you have 20 or more years of experience.

Under FERS, you can retire between ages 55 and 57 (depending on your birth year) if you have 30 or more years of service.

Regardless of your FERS or CSRS status, if you’re 65, you’ll qualify for Medicare. You’ll also qualify for Medicare if you have a qualifying disability.

If you are under 65 and do not qualify for Medicare, you can receive your FERS or CSRS benefits but will have to wait until you reach the Medicare qualifying age of 65.

Social Security Benefits

You must pay into the Social Security program for 40 quarters (credits) in your working life to qualify for benefits. You can earn up to four credits each year.

The amount you receive is based on your earnings history, the year you were born, and the age you start to claim benefits.

Benefit amounts are reduced if you start drawing benefits before your full retirement age which is currently age 66. You can start drawing benefits as early as age 62, but payments can go up by as much as 8% for every year you wait.

Spouses who didn’t work or accrue enough benefit quarters can get benefits based on their spouse’s work record.

Also, when a spouse dies, the surviving spouse is entitled to their own benefit amount or their spouse’s benefit amount, whichever is higher.

Driving Directions to Medicare Health Benefits in Tucson, AZ

Finding Medicare Health Benefits at 2716 S 6th Ave, Tucson, AZ 85713 is easy, no matter where you’re coming from in Tucson or the surrounding areas. Our office is conveniently located in South Tucson, just minutes from I-10, Downtown Tucson, and major local roads.

From Downtown Tucson (Approx. 5 minutes)

- Head south on S 6th Ave toward 22nd St.

- Continue past Silverlake Rd and Interstate 10.

- Our office is located on the right, just before Ajo Way.

From East Tucson (Near Davis-Monthan AFB / Pantano Rd) (Approx. 15-20 minutes)

- Take Golf Links Rd west toward Alvernon Way.

- Turn right on S Alvernon Way and continue south.

- Merge onto I-10 W via the ramp to Phoenix.

- Take Exit 262 for 6th Ave and turn left (south) onto S 6th Ave.

- Drive about 2 miles, and you’ll find us on the right before reaching Ajo Way.

From the Southside (Green Valley / Sahuarita) (Approx. 25-30 minutes)

- Take I-19 N toward Tucson.

- Merge onto I-10 E toward El Paso.

- Take Exit 262 for 6th Ave and turn right (south).

- Continue 2 miles south—we’re on the right, just before Ajo Way.

From the Westside (Tucson Estates / Gates Pass) (Approx. 15-20 minutes)

- Take W Ajo Way (AZ-86 E) toward S 6th Ave.

- Turn left on S 6th Ave.

- Our office is just a few blocks north, on the left.

From Marana & Oro Valley (Approx. 25-30 minutes)

- Take I-10 E toward Tucson.

- Use Exit 262 for 6th Ave and turn right (south).

- Continue on S 6th Ave for 2 miles—our office is on the right before Ajo Way.

Landmarks & Nearby Locations

- Close to I-10 & Ajo Way

- Near South Tucson’s shopping & dining

- Easy access from Silverlake Rd & Benson Hwy

Need help finding us? Call (520) 760-6223 for directions!

Contact Us

Our team at Medicare Health Benefits is here to help, call us at 520-760-6223 any time to schedule a free benefits review.